Taxable Total Return 4th Quarter Review

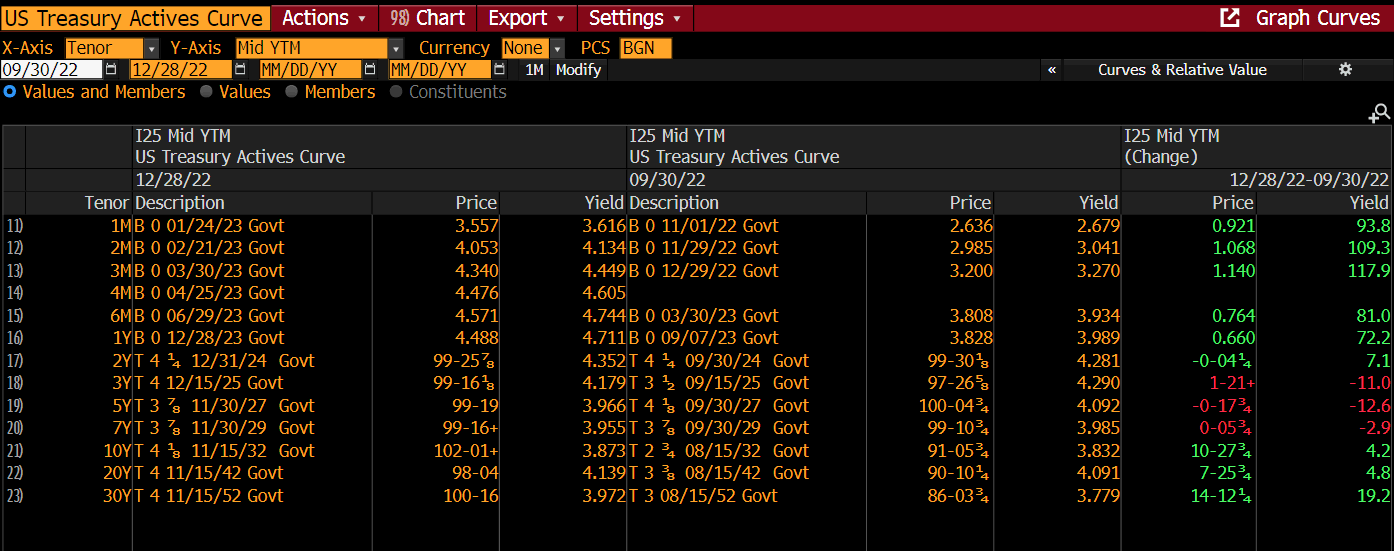

Treasury yields experienced a high level of volatility during the fourth quarter as market participants attempted to predict when the FOMC will end the hiking cycle. At the peak on 10/24/22, the 10-year Treasury reached 4.244%, and the 30-year rose to 4.38% before falling to quarter lows of 3.419% and 3.432% respectively on 12/7/22. Yields have since drifted higher, with the 10-year at 3.88% and the 30-year at 3.976% as of 12/28/22. You can see the net result of the volatility in the Treasury market in the chart below, which shows the change in yields form 9/30/22 to 12/28/22.

Source: Bloomberg

Despite the volatility, spreads on investment-grade corporates and taxable municipals dropped during the quarter. The Bloomberg US Corporate Bond Index was down 29 bps to +130 bps as of 12/28/22. Meanwhile, the spread on the Bloomberg Taxable Muni US AGG Index declined 13 bps to +126 bps during the same time. This trend benefited our strategy, since we have higher combined exposure in spread securities such as taxable municipals and corporates, while we maintain a lower exposure to Treasury securities relative to the benchmark.

During the quarter, we looked to take advantage of the higher yields by extending our duration to the 6.50–7.00 range. Wider spreads and longer durations hurt our performance for most of the year, but that exposure started to benefit our strategy during the final quarter. The tax-free municipals that we bought at the end of Q3 also started to help our strategy as municipals outperformed taxable bonds during Q4. We continued adding to those positions at the beginning of Q4 and are maintaining that exposure going into 2023. It is our belief that these securities will continue adding value and have less volatility than the taxable fixed-income space is currently experiencing.

As we move into 2023, we will look to continue increasing the book yield on portfolios by swapping out of lower-book-yield securities. We expect the volatility in the market to continue into next year until there is more clarity on when the FOMC will stop raising rates. It is our belief that the volatility will create attractive opportunities such as the crossover buying into long tax-free municipals that helped our strategy during the quarter, and we will continue searching for those opportunities going into the new year.

Daniel Himelberger

Portfolio Manager & Fixed Income Analyst

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.