This is part 2 in a series on interest rates and yield curve controls. Here’s the link to part 1: https://www.cumber.com/cumberland-advisors-market-commentary-interest-rates-and-yield-curve-control-part-1/

First, we want to thank BCA Research and our friend Caroline Miller, Chief Strategist at BCA, for permission to share their charts. At Cumberland, we use BCA Research. My colleague John Mousseau and I regularly look at nearly everything they produce. In our annual internal Cumberland voting system on research, they score at a high level.

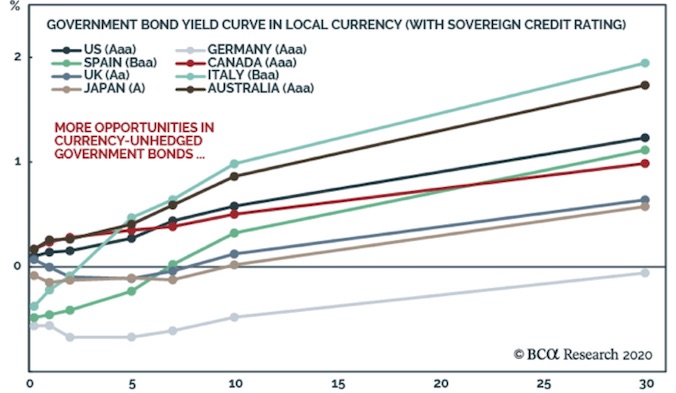

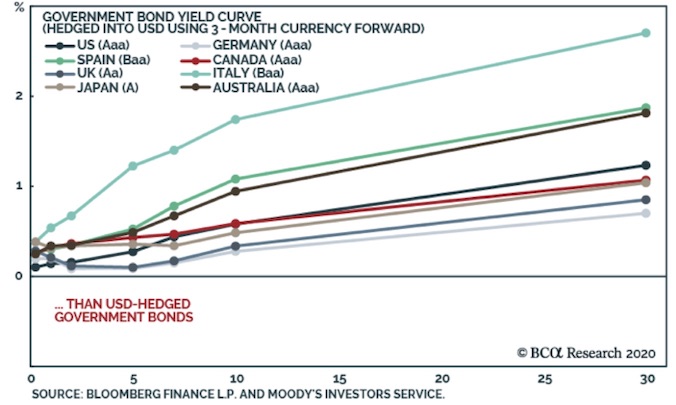

The charts below depict eight countries’ yield curves. One chart is the raw nominal yields, and the other is the same series with currency hedges (the three-month forward rate is used), so that one can see the same yield curves in US dollar terms. There are six currencies here. The credit ratings are different, so some adjustment needs to be made in this comparison for credit risk. Example: Italy and Germany use the same currency (the euro) but are viewed quite differently in terms of credit risk. We could add credit default swap pricing to adjust for credit risk, but it would make this a very complex discussion. So we are keeping it simple for readers’ ease.

Please note how the currency hedge addition to the chart allows a reader to see the somewhat parallel nature of the adjusted yield curves. This is very important. The currency adjustment process is complex but necessary so as to make government debt in various countries available for international investors. The linking to the US dollar is done because the dollar serves as the world’s reserve currency and denominates about 60% of the monetary reserves of the entire world. The second largest reserve currency is the euro. Also note how the widening of the differentials in these yield curves occurs with the countries that carry the lowest credit ratings. Markets are pricing credit risk by a term structure, as you would expect. Thus Italy and Spain lose their parallelism with Germany as the maturities extend on the yield curve. Also, note how Germany’s nominal yield curve is entirely in a negative rate structure. Note that after the currency hedges are applied, the negative rate structure adjusts to a closely parallel term structure when compared to the United States.

Note also how the hedged position yields are bunched together in the shorter-term end of the yield curves. That is due to the worldwide concentrated use of currency hedges in the shorter maturities. Financial market agents use the shorter-term for currency hedging because it is cheaper for them to “roll” the hedges than to add or incur the cost of more extended currency risk mitigation.

There is about $700 trillion in notional derivatives in use worldwide. They are used by businesses, investors, institutions and governments as a means to stabilize transactions among diverse currencies and at various maturities. This is a daily, highly active transactional linkage. To put this into a perspective, the market value of all of these notional derivatives is estimated to be $15–20 trillion. Think of that as a functioning market of enormous size that you do not see every day on your screen. Cumulative data is available, with a large time lag. One has to compile it by obtaining reports from all of the world’s largest, systemically important financial institutions. The data is also available from reports provided by BIS (Bank for International Settlements).

The three-month forward currency hedge is very common. Derivative swaps in the intermediate and longer end are based on the differentials in interest rates. So we get a mixed picture, since the currency options are using a “rolling” three-month hedge while the lending portions are using a more closely aligned maturity-matching regime. Nearly every major, systemically important (SIFI) bank in the world is involved in this process every single day.

For bond investors, it is critical to understand the movement in the US Treasury bond markets in the global context of currency-hedged investment-grade interest rates. They are critical for the US muni market and the investment-grade corporate market. As bond managers we have to watch these relationships every day. Otherwise the price and yield movements in a single market can make no apparent sense. After the currency hedge adjustments and the derivative adjustments (those are coming in part 3) are taken into account, market-based interest rates make a lot of sense. It is that trajectory that gets us to the interest rate outlook and to the question of yield curve controls.

We’re working on part 3 of the series now.

David R. Kotok

Chairman of the Board & Chief Investment Officer

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Sign up for our FREE Cumberland Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.