During an August 14, 2020, lecture at the Center for Financial Stability, Charles Goodhart (former member of the Bank of England’s Monetary Policy Committee and professor at the London School of Economics) mused about the US’s current economic slowdown and the prospects for inflation that might result because of the extraordinary increase in the money supply that has occurred (http://centerforfinancialstability.org/research/Goodhart_Deflation_Inflation_081420.pdf).

![]()

After reviewing history, Goodhart turns to a discussion of where we are now. He makes three points. First, policy is currently expansionary, with low interest rates. Second, the pandemic has resulted in a shock to both aggregate demand and supply, and the path of the recovery is as yet uncertain and critically dependent upon a vaccine. Third, inflation will remain low for a long time. However, he then notes Milton Friedman’s classic observation that “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” (Milton Friedman, “The Counter-Revolution in Monetary Theory,” IEA Occasional Paper No. 33, 1970; https://miltonfriedman.hoover.org/friedman_images/Collections/2016c21/IEA_1970.pdf.

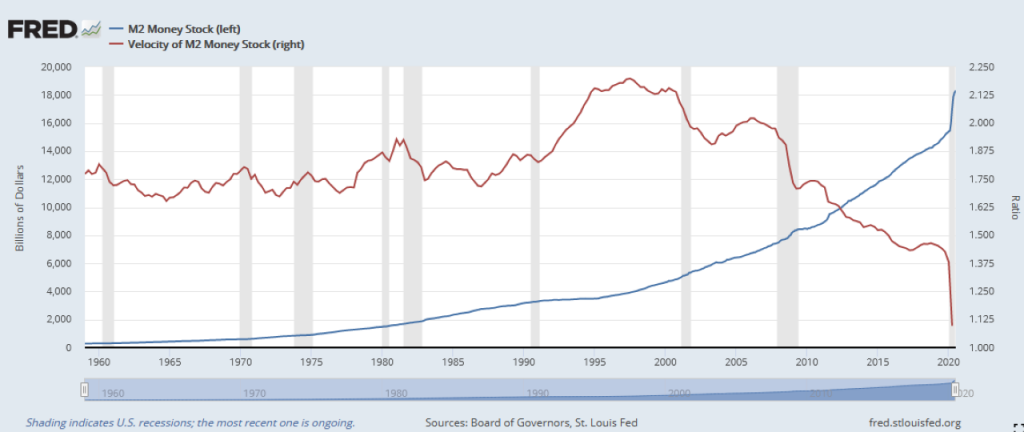

Goodhart notes that monetary growth has surged by some 32% in early 2020, and to a monetary economist this means that future inflation is almost a certainty. The timing is uncertain and depends on what happens to the velocity of circulation. As the chart below shows, the decline in velocity in the short run has offset the money supply increase, due in part to a large increase in precautionary saving and a drastic cut in aggregate demand for many goods and services.

Robert Eisenbeis, Ph.D.

Vice Chairman & Chief Monetary Economist

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Sign up for our FREE Cumberland Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.