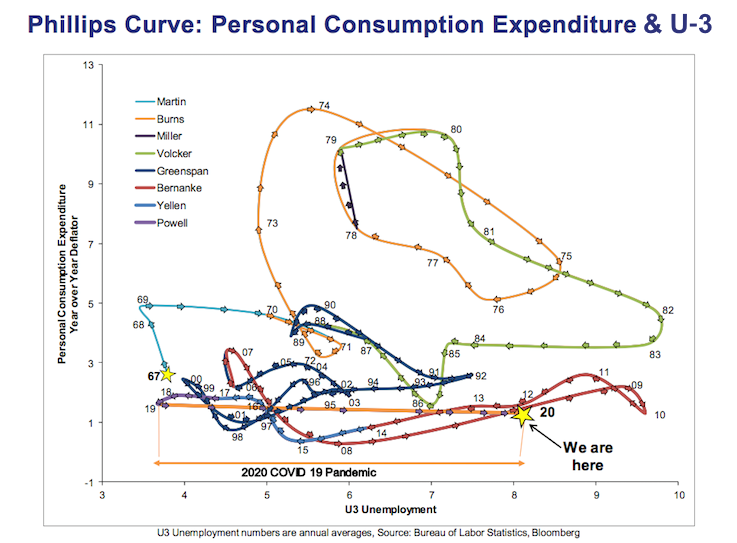

We created the chart below to depict an “underdamped oscillatory system.” Hat tip, Dr. Thomas Synnott III.

We’ve included a half-century of Phillips curve data for personal consumption expenditures (PCE) vs. U-3 unemployment, color-coded by the person who was Federal Reserve chair at the time. That way you can see a year-by-year history for all Fed chairs since William McChesney Martin. We’re using the PCE to describe inflation, since it is the Fed’s preferred inflation measure (https://www.dallasfed.org/research/pce). We’re using the traditional unemployment rate (U-3) since the Fed refers to it in their forecasts (https://www.bls.gov/news.release/empsit.t15.htm).

The horizontal orange line that links year 2019 (19) to year 2020 (20) depicts the effect of the COVID shock of last year, when U-3 unemployment more than doubled from under 4% to greater than 8%. As you can see, there has been nothing in modern history like this sudden surge. The violence of the shock is greater and more abrupt than in any of the crises in the entire time period depicted.

Our point is to support what we are hearing from Fed Chair Jay Powell. This is on his watch and the challenge for the Fed is monumental.

There are all sorts of warnings and forecasts of inflation spikes coming from the collective punditry. They may ultimately be correct, but is an immediate inflation spike on the horizon? We don’t think so. A temporary rebound is not an inflation shock that triggers a permanent trajectory shift in the price level. So for now, we view this economic recovery as coming from a “hundred-year-flood” type of shock.

Note that the shock you see depicted does not include the imminent substantial demographic shift of nearly a million dead Americans in excess of “normal” numbers. Nor does it show the global shock from “excess” deaths in nearly every other country. It also does not show the results of a growth-penalizing Trump administration policy that limited US population growth by restricting immigration. All that will unfold in 2021 and beyond.

Nor does the chart show the now-developing healthcare shock as long haul COVID illness threatens a growing cohort of people. In America the estimate of long haul COVID cases hovers around 10 million; it may take years for us to really know how large this cohort is. In other parts of the world the per capita estimates may be much higher, since developing world healthcare systems are not as deep as ours. We are only just starting to see that “long hauler” statistical base evolve.

Our first conclusion is that the “shadow” unemployment rate estimates are much closer to COVID reality than are the traditional BLS estimates (see for instance http://www.shadowstats.com/alternate_data/unemployment-charts). We believe U-3 may actually be in the 11%–12% range. You can see this figure supported in employment population ratios and in labor participation rates.

Our second conclusion is that the current GDP recovery is being driven by Covid lockdown forced productivity gains achieved through technological innovation instead of by adding people to the labor force, which means deflationary pressures in many places. Many of those gains are permanent shifts and not transitory. That’s deflationary, not inflationary.

For other views that readers might want to consider, we recommend the following:

1. “Understanding the Size of the Government Spending Multiplier: It’s in the Sign,” Federal Reserve Bank of San Francisco, https://www.frbsf.org/economic-research/publications/working-papers/2021/01/

2. “Inflation fears and the Biden stimulus: Look to the Korean War, not Vietnam,” by Joe Gagnon, Peterson Institute for International Economics, https://www.piie.com/blogs/realtime-economic-issues-watch/inflation-fears-and-biden-stimulus-look-korean-war-not-vietnam. Also by Joe Gagnon, “Bond yields are not good predictors of inflation,” https://www.piie.com/blogs/realtime-economic-issues-watch/bond-yields-are-not-good-predictors-inflation

3. “Is Inflation Coming?” Money and Banking, https://www.moneyandbanking.com/commentary/2021/2/14/is-inflation-coming

The investment implications for a productivity-growth-driven low inflation and a low-interest-rate environment are significant. We remain overweight the healthcare sector (long haulers need care), the materials sector for infrastructure buildout and economic recovery, ESG, and other sectors where the longer worldwide recovery cycle ahead will deliver a post-shock world different from the one we knew pre-COVID.

This is NOT a “normal” recovery cycle, so using normal indicators may be a trap. For confirmation, just take another look at the chart at the top of this missive.

David R. Kotok

Chairman of the Board & Chief Investment Officer

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Sign up for our FREE Cumberland Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.