We see more and more payment liabilities revealed as the FTX affair unfolds. Successive bankruptcies make headlines. Lawsuits originate against sports personalities and celebrities who garnered fees for advertising themselves as endorsers or supporters within the crypto space. This is what happens when there are as many as a million claims globally that originate from folks who have lost money.

Please remember that many lawyers in this space work on contingent fees, so the incentives are in place to find ways to recover damages in lawsuits. And the various legal jurisdictions span the globe.

The FTX affair we see unfolding is an example of a slow-moving possible contagion. So far. Let’s not forget the infamous quotation in the famous Hemingway novel The sun Also Rises. A character named Mike is asked about the way in which he went bankrupt. “Two ways,” he answered. “Gradually, then suddenly.”

My colleague Bob Eisenbeis, Cumberland’s Chief Monetary Economist, whose credentials include a distinguished career at the Federal Reserve, wrote as follows:

At present, there are over 9,300 cryptocurrencies in existence, and they operate internationally in hyperspace, that implies over 40 million possible exchange rates if one wanted to convert from one currency to another. This is compared with 180 government-sponsored currencies in the world, requiring about 15,000 exchange rates.

The crypto industry has expanded and is now quite complex. It includes issuers, exchanges, specialized hedge funds, banks, and securities firms, plus crypto-based investment vehicles such as ETFs. While some skeptics, Jamie Dimon among them, have voiced reservations about cryptocurrencies, at the same time their firms, including JPMorganChase, Morgan Stanley, and Goldman Sachs, have quietly entered various aspects of the cryptocurrency business. Even the Federal Reserve Bank of New York has created a 12-week pilot program based upon a digital dollar-based blockchain system involving participants like BNY Mellon, Citi, HSBC, Mastercard, PNC Bank, TD Bank, Truist, U.S. Bank, and Wells Fargo. Whether the events surrounding FTX will chill this project remains to be seen.

For Bob’s full essay, published on November 25, see “It Isn’t Over Till It’s Over”: https://www.cumber.com/market-commentary/it-isnt-over-till-its-over.

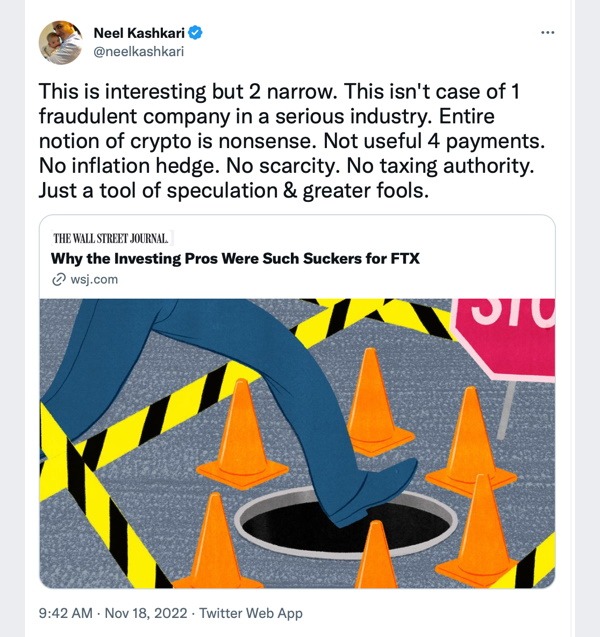

Bob also notes that Federal Reserve Regional Bank President Kashkari didn’t mince words, as reported in the Wall Street Journal. President Kashkari tweeted,

(https://twitter.com/neelkashkari/status/1593615608125526019?s=20&t=Y2gAOl3_Y1ZoWmQSP8Q5cw)

The WSJ elaborated on the points Kashkari made:

• Not useful for payments. One of the primary advantages of circumventing banking systems is for quick, anonymous transactions — even cross-border. FTX's unraveling may call into question how effective crypto's 'decentralization' really is. We recommend the article in full.

(“Fed's Neel Kashkari Lambasts Crypto,” https://www.wsj.com/livecoverage/stock-market-news-today-11-18-2022/card/fed-s-neel-kashkari-lambasts-crypto-u0wRqdn2yy6d09V4hvFi)

Here’s a single example of a market-based pricing reaction function. This one involves a US publicly traded security with which many are familiar. The symbol is COIN. As this note is written (December 3), the stock price of COIN has declined from around $280 peak in the last year to around $43. As to the future for this stock, there are all types of forecasts, ranging from a very bullish buy recommendation (it will more than double from this current level) to dire predictions of more contagion carnage and a debacle.

Readers can sort those out for themselves.

When we started drafting this note, we asked our colleague Dan Himelberger for the details on the five issues of Coinbase debt. Below is a screenshot from his Bloomberg terminal on one of the issues so that readers can see the history and ratings. (Note this is about 2 weeks old) Dan notes that this screenshot is just one of the five debt issues.

The second screenshot is the trading history. Note that the history of the trading yield on the Coinbase bond coincided with a period of rising interest rates, so we would normally expect to see some downward market price adjustment as all seasoned bonds declined in market price during a period when interest rates were rising in the new-issue bond markets.

But this decline was taking the bond market value of this bond to about 50 cents of the face-amount dollar. And that is on a bond maturity in about eight years at par. So if you bought this bond at 50 cents on the dollar two weeks ago and you end up getting paid, you will double your investment while also obtaining the regular coupon payments of interest. Note that the credit ratings were in the high-yield category and that they also were at the very highest level within the junk bond sector. In our opinion, the market-based pricing of this bond without the overhang of crypto and FTX fallout would certainly be much higher than 50 cents on the dollar.

We will leave it to readers to determine any action to take. Cumberland does not own this bond in managed accounts.

We also note that the bond has not defaulted. Whether it will do so remains to be seen.

The impact of the price changes in the stock and the bond are seen directly in these securities. They are also seen indirectly in traditional mutual funds and in the ETFs and other portfolios that hold them. How much impact requires a case-by-case analysis. The point of today’s note is that there is some slow moving contagion going on and that it may be obscure for some investors. The tentacles of the FTX affair reach far beyond the Bahamas regulator.

We again remind readers that Cumberland does not hold this bond in managed bond accounts. And we do not own Coinbase stock in our managed equity or ETF portfolios. There is some possible exception since there may be some COIN in a broad-based ETF that contains many issues. Cumberland has avoided the financial sector ETFs that have any heavier weightings of crypto exposure.

One last note.

The FTX affair is an example of how the G (governance) factor in the ESG rating system helps investors. Transparency is a positive ESG principle; opacity is its opposite and a negative ESG rating mark when using an ESG rating scheme. Credit structure and auditing standards are positive principles; a lack of them is another negative. Regulatory discipline is a positive principle; poor regulation and politically driven culture war assessments are negative principles. All of these are aspects of the help that the ESG factor rating principles give an investor. In the case of FTX those principles helped investors who used them properly to avoid a disaster with FTX. In my opinion, ESG tools add alpha to an investor in two ways: They help seek benefits within market sectors and industries, and they help avoid damage by suggesting items to review for risk.

More with be forthcoming as the FTX affair develops as the latest in the saga of investing behaviors. We’re currently focused on the sector of stablecoins that are supposedly linked to a fiat currency. We are watching to see if there evolves a situation in which a token that was supposed to be 100% backed by real money turns out to have insufficient collateral or another form of deficiency in linkage to the promised currency.

David R. Kotok

Chairman & Chief Investment Officer

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.